MLCC Super Cycle?

The smallest component in the datacenter is becoming the biggest bottleneck.

The views in this article do not represent views of any past, present, or future employer.

All models, projections and opinions are for educational purposes only. This is not financial advice.

Before even saying hi, three pieces of information. They'll write this article by themselves.

The four major manufacturers of Multi-Layer Ceramic Capacitors (MLCC) have been consistently increasing their lead times. Ranges go from 10 to 30 weeks.

A single Vera Rubin NVL72, the new NVIDIA flagship GPU rack, with 72 GPUs could contain upward of 1.5–2 million Multi-Layer Ceramic Capacitors.

Murata, the giant of Multi-Layer Ceramic Capacitors, starting this week, on 1st of April has adjusted its prices and reported capacity of production in all its lines of 98%. Samsung Electro-Mechanics the other big player on the MLCC Field is, of course, doing the same.

But before we keep talking about capacitors demand, and prices, let’s refresh what it is and why it matters.

What is a MLCC?

You probably know this but if not, a capacitor is a tiny box to store energy, it is not more than that. How is it different from a battery? Well it stores smaller amounts to be released very fast, while going to a power source takes more time. So the capacitor sits next to the components that need power, loaded up, otherwise it would cause glitches or crashes. Basically if you have a component that you don’t want that gets fried you put a capacitor to provide it with power.

An MLCC, or Multi-Layer Ceramic Capacitor, is a kind of capacitor that is smaller than a traditional one and it’s made of tiny layers of ceramic (thus the name) between electrodes, and that ceramic is what allows energy to be stored between the layers.

Ok and why a capacitor matters? It is basically in every electronic piece of the world, from your microwave to those multi billions datacenter, and they are controlled in a duopoly by two companies.

Who is who

On the MLCC game there are two big names, almost a duopoly, that depending on who you ask control between 70 and 80% of global market. This duopoly gets bigger on the super specialized AI sector.

Those are Murata Manufacturing (TYO: 6981) and Samsung Electro-Mechanics (KRX: 009150). They are not alone of course, they are in good company of Taiyo Yuden (6976.T), smaller than the two former but focused on the AI demand, TDK (6762.T), riding the electric vehicles wave and on the Chinese play Fenghua Advanced Technology (000636.SZ) China’s MLCC volume champion, one of the most leveraged in margins on the MLCC sector.

All of them as on my initial line telling their customers “You have to wait, we are out of capacity”.

But why?

Well there is no single thing that explains it but a multi factorial one that makes this different, (yeah the favorite investors phrases) than previous cycles.

The racks of chips used on the datacenter are becoming power hungrier, every new architecture consumes more power than the previous therefore more capacitors are needed. The new Rubin architecture of NVIDIA can 2.5x or 3x the number of MLCC needed, and we are talking per rack not about new capacities installed. So do the math more capacitors per racks, more racks per each new datacenter. if it is white and it is in a bottle, it is probably milk.

A traditional gas car uses 3,000-5,000 MLCCs. An early Tesla Model 3 used around 9,000. Modern Tesla uses 15,000-17,000, and there are already estimations of self driving cars can add 5,000 MLCCs more. The estimate for 2030 of EV sold is around 40-45 millions. Just a comment to add to this, few days ago NVIDIA signed a deal with Uber for robotaxis.

The global drone industry produces over 10 million units annually across consumer, commercial, and military segments, collectively consuming an estimated 1.5–2.5 billion MLCCs per year. The 2030 projection is more than 20 million units.

Japan, Korea and specially China are pushing rapidly efforts for developing humanoids and ramping up more and more robots, Elon Musk is talking about deploying only from his Optimus 1 million of humanoids for 2030. But even if that is an overestimation and only half are deployed between Asia and Tesla, a complex humanoid can take even more MLCC than a traditional electric vehicle. Are you adding up?

Now sum all that with the traditional demand of electronic, industry, IoT, Edge Computing, video games and phones.

It sounds like a perfect cocktail for a shift from a cyclical component to a structural demand, but hey, there is still April of 2026 people calling the memory demand a cycle.

The smallest component in the datacenter is becoming a real bottleneck.

For this piece and this might be the beginning of a series I want to focus on Murata, not as a whole company but only their MLCC division.

Murata

They are the MLCC leader, a Japanese firm of ¥7.35 trillion market cap, their product lineup goes from capacitors, inductors, resistors, and thermistors, through RF/wireless components to power products, batteries, sensors and even micro-mechatronics. They have been using their core business on MLCC to diversify and becoming vertically integrated in the electronic industry.

Murata accounts from 30-35% of the global MLCC market, and a few interesting have been happening lately, worth watching all of them.

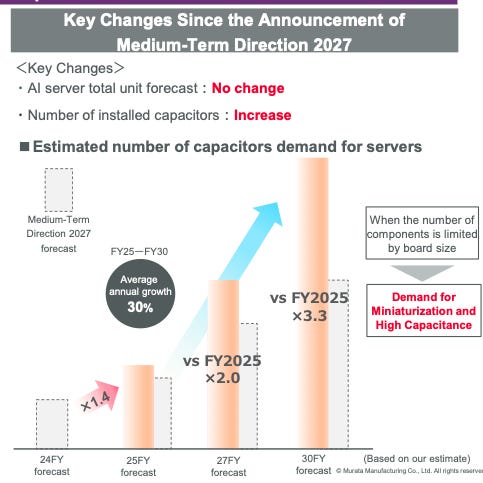

In Murata’s IR Day presentation from December 2025, the company projects that server capacitor demand will reach 3.3x FY2025 levels by FY2030, growing at a 30% average annual rate. They also revised upward the number of MLCCs per AI server baseboard from 10,000–20,000 to 15,000–25,000.

However, the slide is explicitly clear on one critical point:

AI server total unit forecast: No change

This means the entire 3.3x growth comes from more capacitors being installed inside each server, not from more servers being built. Murata is assuming zero growth in the number of AI servers deployed worldwide, which contradicts every headline, every other CEO in the world, every new GW secured for a new datacenter, but it is a Japanese company so hard sandbagging is expected. I know there's a lot of noise around datacenter buildout, that the 200 GW target for 2030 might never happen, but even if you add just 40 GW of capacity over the next few years, the demand for AI MLCCs will still suffer an explosion.

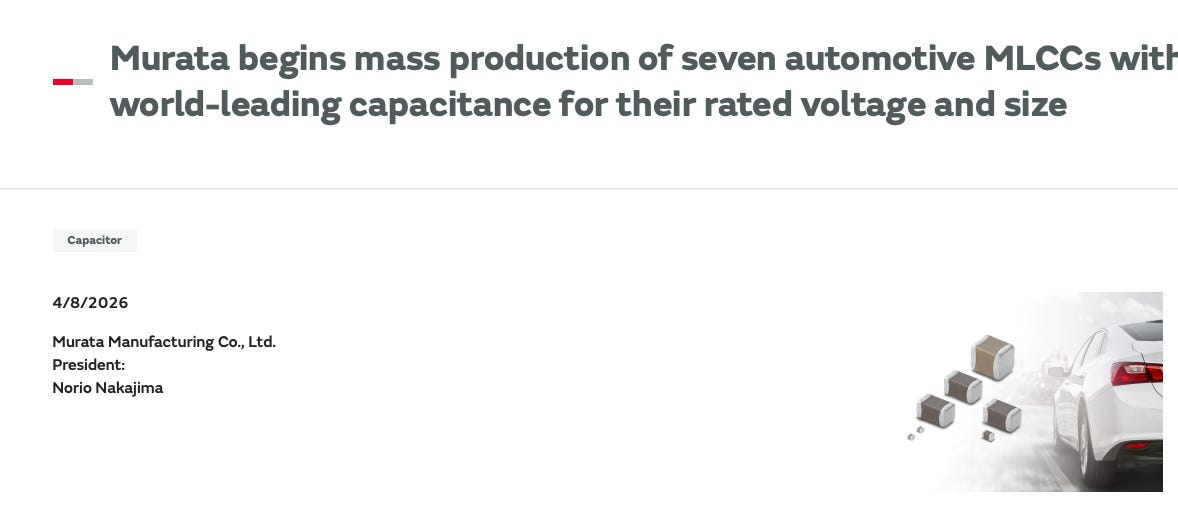

Few days ago Murata launched seven new miniaturized components designed for self-driving and driver-assistance systems. These capacitors pack more energy storage into smaller packages, so engineers can fit more computing power onto circuit boards without running out of space. As vehicles get increasingly packed with sensors and processors, demand for these components keeps surging. One of those low voltage is the model GCM035D70E225ME02. The advance helps automakers build smarter cars while using fewer parts and less board space.

Murata is preparing for a high expansion of their production lines for their MLCC lines. Murata Electronics (Thailand) completed a production building in March 2023 after starting construction in July 2021. The Iwami Plant (Hane) at Izumo Murata in Japan finished in April 2023 from a March 2022 start. Wuxi Murata Electronics in China completed its production building in April 2024 after breaking ground in November 2022. Fukui Murata Manufacturing in Japan wrapped up an R&D facility in February 2026, having begun in December 2023. Most recently, Murata Electronics (India) signed a lease in February 2025 for a rental factory with packaging and shipping capabilities, aiming for full-scale operation in FY2026.

Does it sound like they think this demand is stopping any time soon? You don’t build such capacities thinking of cycles, right?

Although this is not directly about capacitors but Murata started to develop sensors for drones like SCH16T Series, so they are participating in the whole supply chain of the new demands.

Humanoids

You might think I am jumping to other business areas, but I am not. It gets interesting because I think Murata is doing something quite clever. They are developing or co-participating in different product lines to diversify, but at the same time making sure those new lines feed their main business, which is capacitors and inductors.

But before going there a small piece of news, from couple of weeks ago, on March 24, from Japanese press.

NEDO opened the call for proposals for a completely new program: “AI Robot / Physical AI Multimodal Foundation Model Development” (AIロボット・フィジカルAIを見据えたマルチモーダル基盤モデル開発事業).

This is separate from and on top of the existing ¥20.5B data platform. The framing is significant: NEDO states that “the necessity of domestically developed AI multimodal foundation models that can protect on-site data while being safely utilized in the future is increasing,” and the program aims to develop foundation models serving as the base for AI robots and Physical AI, strengthening Japan’s industrial competitiveness in manufacturing.

Connect that information with this: Murata is a founding member of a 13+ organization consortium established in June 2025, called KyoHa (Kyoto Humanoid association), this entity aims to address challenges in Japan’s humanoid robotics field, such as the lack of a domestic hardware development framework and the absence of an integrated industrial structure. The members include Tmsuk, Waseda University, Mabuchi Motor, Kayaba (KYB), NOK, Sumitomo Heavy Industries, Renesas, JAE etc.

So Japan is telling they need to secure their humanoids sovereignty and Murata is sitting in the middle of that. More humanoids more MLCCs. The math is not hard.

It is obvious Murata is acting actively in all parts that will matter in the future, EVs, AI servers, drones and humanoids.

But it does not end here

BaTiO3 and Murata's MLCC Moat

I want to mention the supply chain, because this also puts Murata in a very interesting position. Ceramic dielectric powder (BaTiO₃) is the core material when producing this kind of capacitor, they represent 35-45% of high-cap MLCC costs.

Murata produces its own BaTiO₃ dielectric powder at 100nm particle size. Korean manufacturers are at 300–500nm. This is a 3–5x gap in the raw material that determines everything downstream.

Not the whole industry produces its own BaTiO₃; it is also purchased on the merchant market. Sakai Chemical Industry holds around 25–30% of the market and is Japanese, same as Nippon Chemical Industrial, which controls around 15% of the global supply. So Murata’s supply chain of ceramic powder is at home, without depending on geopolitics or currency risks. Additionally, in 2013 Murata formed a joint venture called MF Material with Ishihara Sangyo Kaisha and Fuji Titanium Industry, with the purpose of securing raw material procurement of barium titanate for MLCCs.

The real story is vertical integration depth. Murata controls from BaTiO₃ powder through finished product.

Internal electrode (nickel powder/paste) also represents 15–25% of the final product and accounts for about 9% of MLCC cost. This is 100% merchant market; not vertically integrated by MLCC makers. Nickel powder prices rose 15% in 2025 and another 15–20% in early 2026.

If you enjoy these articles or find them useful, share them. Substack buries free posts so the only way this reaches anyone is you send it.

Modeling the MLCC area

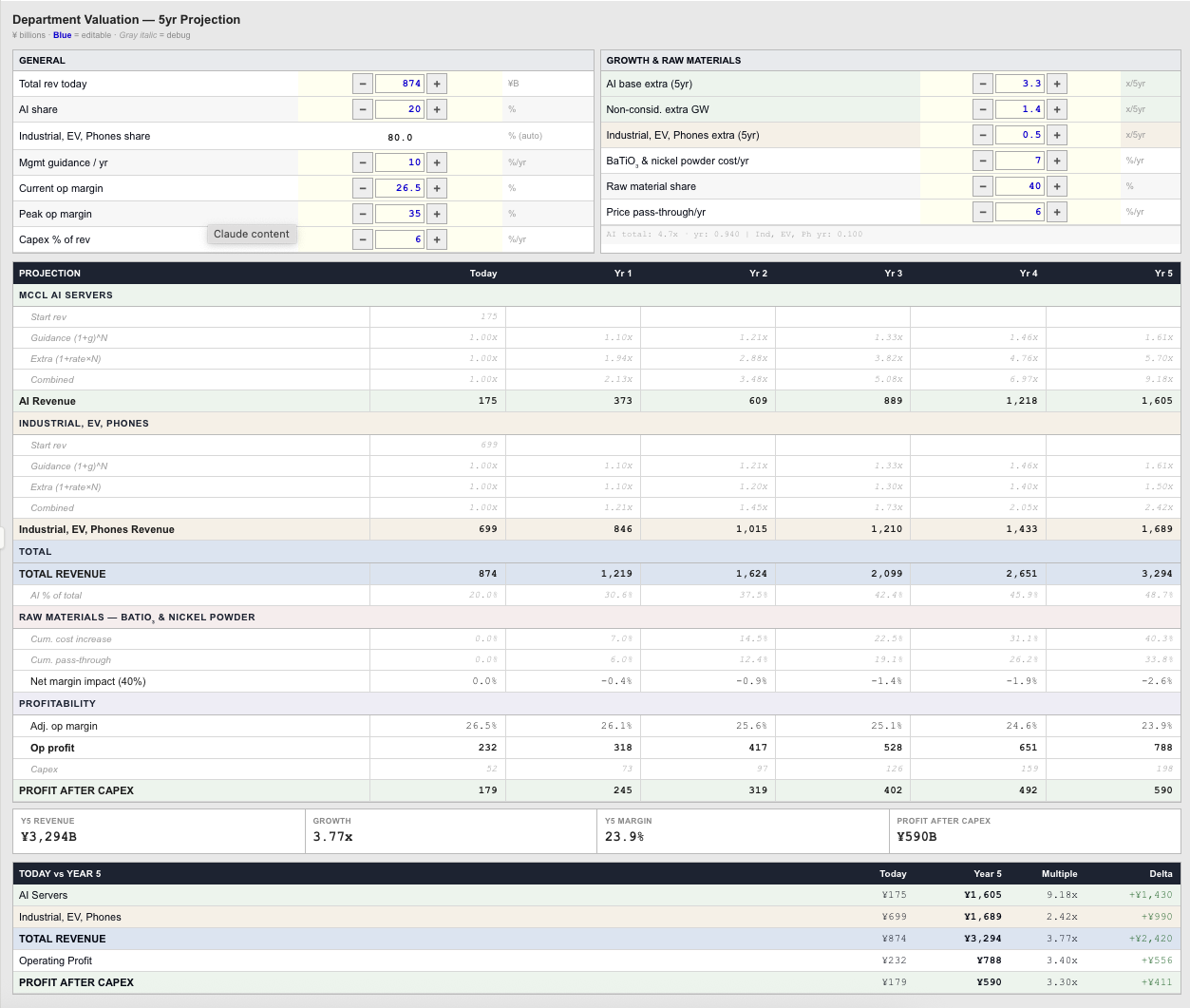

I built a model only for the MLCC area, ignoring the rest of the company, as an educational exercise, starting from the existing ¥874B. My assumption is 20% of MLCC revenue is AI and the rest 80% is industrial, phones, and EV.

This does not constitute any financial advice, it is pure fun and education..

I made a bull case assuming the 3.3x will apply only to the 20% of MLCC and will compound per year. I am also factoring in new capabilities and new GWs installed, because every major economy is racing to build power capacity right now, from the US adding gas and nuclear for data centers to the Middle East and Southeast Asia building out grids from scratch, and every single one of those gigawatts needs MLCCs in the power electronics that manage it. I assume Murata will have a secure source of raw materials and will be able to pass up to 6% price increases.

Again, those are just assumptions. I don't have access to IR, and a model, as you know, is only as good as your assumptions and your sources of information. Mine are purely public information, guesses, and hours of trying to reverse-engineer bills of materials of Tesla's cars or NVIDIA's chips.

In my bull case, with 1.4x extra GW and 6% capex, the MLCC department goes from ¥874B to ¥3,294B in five years, a 3.7x. AI Servers scale from ¥175B to ¥1,605B (9.18x), nearly half the department’s revenue by year 5 at 48.7%, up from 20% today. Industrial, EV, and Phones grow from ¥699B to ¥1,689B (2.42x). Operating profit goes from ¥232B to ¥788B (3.40x) and profit after capex from ¥179B to ¥590B (3.30x).

Margin still compresses to 23.9% from the BaTiO₃ and nickel powder cost gap, but the AI volume explosion more than makes up for it.

Is this a recommendation of anything? No. This does not mean anything for the rest of the company's business and all my assumptions can be terribly wrong, not one new data center built and AI racks replacement stale.

Just a tangent comment, it always amazes me, how projections can be done of an entire company for 10 years. It is really hard what can ever happen next year with any technology imagine trying to predict how the AI industry or semiconductors will look in 10 years

And that takes me to the risks

Can it go wrong?

Short answer: of course.

First the most obvious, AI Buildout stop. Hyperscalers stop. The AI story goes to hell. No datacenter no racks no Murata new MLCCs.

But if that goes well you get the commoditization of the mid-to-low-end market. As with any super cycle, when high-end AI servers and automotive MLCCs command premium pricing and consume production capacity, manufacturers prioritize those lines. The industrial and consumer segments get deprioritized, and that vacuum is exactly where Chinese manufacturers step in. Fenghua, Sanhuan, and other domestic Chinese producers have been aggressively expanding in medium-size, low-capacitance products, and their global revenue share is increasing.

Worth considering that the memory shortage cascading to consumer electronics. The AI infrastructure buildout is consuming semiconductor capacity across the board, not just GPUs but memory, substrates, and advanced packaging. If HBM and DRAM shortages worsen, consumer device production could slow. Apple is reportedly securing memory supply aggressively, but there is no guarantee this insulates the broader smartphone market, and this is something important to clarify: the only disclosed customer exceeding 10% of revenue on EDINET filings is Hongfujin Precision Electronics, which is Foxconn's iPhone assembly subsidiary. This is literally an Apple proxy. So a slowdown in iPhones means less Murata cake.

Every MLCC super cycle in history has ended. The 2017–2018 cycle saw prices rise 5–10x followed by a sharp correction. The current cycle is structurally different, driven by AI infrastructure rather than smartphone demand, but the pattern of overshoot and correction is deeply embedded in this industry. The model assumes price increases persist through FY2031, but a correction is plausible if capacity additions catch up to demand.

And?

This is just a personal opinion, but MLCC is a structural change in demand, not a cycle.

Every previous MLCC boom was tied to a single consumer product: smartphones in 2017–2018, tablets before that. This one has four or five demand drivers hitting simultaneously (AI racks, EVs, ADAS, drones, humanoids), and none of them are substitutes for each other. The opposite, each new model of AI is an opportunity for a more advanced humanoid, drone, or EV.

All the efforts made in the industry: every ASML machine, every SK Hynix new line of production, every new research in chemistry for substrates, every new NVIDIA architecture is to produce chips that will sit in racks that will demand more capacitors.

Murata sits at the center of that stack with 35% market share, a supply chain denominated almost entirely in yen, upstream vertical integration through the MF Material joint venture, and a management team that just told the world they expect zero growth in AI server units. Given that they’ve revised production upward twice and are raising prices aggressively, it’s a very conservative statement.

Time will tell.

This is not financial advice. My qualifications for financial guidance are exactly zero.

If you enjoy these articles or find them useful, share them. Substack buries free posts so the only way this reaches anyone is you send it.

Sources and further reading

SCH16T-K20 High-Precision 6-Axis IMU for Robotics and Camera Systems

Murata: Earnings Release Conference Third Quarter of FY2025

onsolidated Financial Results for the Nine Months Ended December 31, 2025 (Under IFRS)